While a substantial dividend yield may seem enticing, it often signals underlying risks, as is the case with AGNC Investment (NASDAQ: AGNC) and its whopping 15% yield. In contrast, investors would be wise to temper their yield expectations and consider investing in the out-of-favor Realty Income (NYSE: O), which offers a more modest 5.9% yield but provides greater reliability. Here’s why Realty Income should be favored over AGNC:

- Reliability: Realty Income’s track record of consistent dividend payments makes it a dependable choice for income investors. Unlike AGNC, which carries elevated risk due to its exceptionally high yield, Realty Income offers a yield that investors can count on.

- Stability: Realty Income operates as a real estate investment trust (REIT), primarily focused on owning and leasing commercial properties. This stable business model contributes to predictable cash flows and steady dividend payments, mitigating the volatility associated with AGNC’s mortgage real estate investment trust (mREIT) structure.

- Dividend Sustainability: With a diversified portfolio of high-quality properties and a focus on long-term leases with reliable tenants, Realty Income is better positioned to sustain its dividend payments over time. In contrast, AGNC’s dividend sustainability may be compromised by fluctuations in interest rates and mortgage-backed securities performance.

In summary, while AGNC’s high yield may initially appear attractive, the inherent risks make it a less favorable option compared to the more reliable and stable dividend income offered by Realty Income. Therefore, investors would be prudent to prioritize Realty Income over AGNC for their investment portfolios.

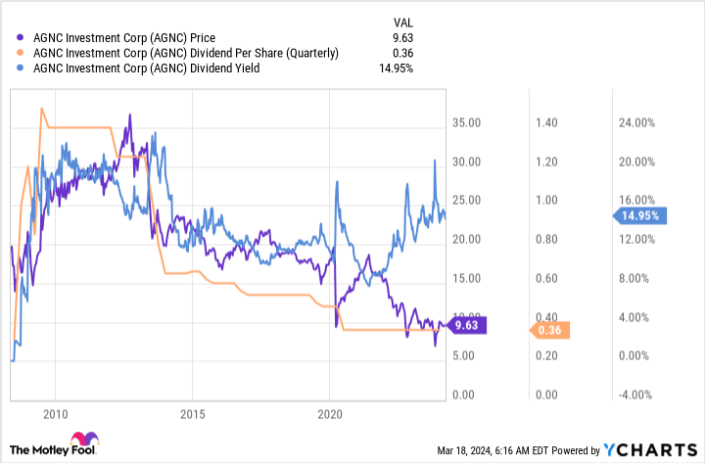

One graph is all you need

The graph depicting AGNC Investment tells a clear story: its dividend has been highly variable and consistently decreasing over the past decade, mirroring the downward trend in its stock price. Despite this, the dividend yield has remained relatively high, driven by basic math, but this masks the erosion of both income and capital for dividend investors. This makes AGNC a poor choice for investors seeking dependable income from their portfolios.

Instead, investors should opt for a reliable dividend stock like Realty Income, which offers stability and consistent dividend payments over time.

Realty Income is a dividend machine

While both Realty Income and AGNC Investment are real estate investment trusts (REITs), they operate in distinct niches within the REIT space. AGNC stands out as a unique type of REIT that focuses on purchasing mortgage securities, a complex and high-risk segment. In contrast, Realty Income adopts a more conservative approach, primarily investing in physical properties that it leases out to tenants.

Realty Income specializes in net lease properties, where a single tenant leases a property and assumes responsibility for most property-level operating costs. While individual properties may carry some risk, the diversification across a vast portfolio of more than 15,000 properties significantly mitigates overall risk. As the largest net lease REIT, Realty Income benefits from its extensive and diversified property holdings, providing stability and reliability for investors.

The yield, at around 5.9%, is near its highest levels of the past decade, which suggests that now is an attractive time to buy Realty Income stock. The first question you should ask is, “Why is the yield historically high?” The answer is that interest rates have gone up, increasing the cost of capital for Realty Income (and other REITs). That is a headwind for sure, but property markets have historically adjusted to interest rate shifts and are likely to do so again.

Meanwhile, Realty Income is the largest net lease REIT by a wide margin. It is more than twice the size of its next-closest competitor, giving it a size advantage when it comes to buying new assets. In fact, it has bought up a couple of REIT peers in recent years, adding industry consolidation to its growth opportunities. Helping the bullish thesis is an investment-grade balance sheet and an increasingly diversified portfolio, including a growing presence in Europe.

The proof of the company’s success is found in the dividend, which has increased for 29 consecutive years. While the annualized dividend growth rate is modest, coming in at roughly 4.3% over that span, it is pretty clear that income investors can count on Realty Income to keep paying through thick and thin. If you are looking for a sustainable high yield, Realty Income is a much better choice than AGNC.

Be careful what you wish for

Relying solely on a stock’s dividend yield can lead to significant pitfalls, as demonstrated by AGNC. Despite maintaining a high yield, AGNC repeatedly reduced its dividend payments, resulting in disappointment for investors. In contrast, history suggests that Realty Income is a much more reliable option for dividend investors. Furthermore, the current situation, where Realty Income is out of favor and offering a historically high yield, presents a long-term opportunity that should not be ignored.

{kind=link}